PPO or HDHP? Making Health Insurance Choices

More than half of large U.S. companies offer employees a high-deductible health plan (HDHP).1 When an HDHP is offered, employees often have a choice between the HDHP and a traditional preferred provider organization (PPO) plan. People who buy coverage outside the workplace may face a similar choice.

Premiums are generally lower for an HDHP than for a PPO, but you typically pay more out of pocket for specific medical services. If you choose a PPO, you may pay less out of pocket for a given service, but you pay more each month for premiums.

Here are some other factors to consider.

Network — PPOs and HDHPs both offer incentives to use health-care providers within a network, and the network may be exactly the same if the two plans are offered by the same insurance company. If you have a preferred physician, it's wise to make sure he or she is included in the network before enrolling.

Maximums — Most health insurance plans have annual and lifetime out-of-pocket maximums above which the insurer pays all medical expenses. HDHP maximums may be the same or similar to that of PPO plans. If you have high medical costs that exceed the annual out-of-pocket maximum, your total out-of-pocket costs for that year would typically be lower for an HDHP when you consider the savings on premiums.

Health Savings Accounts

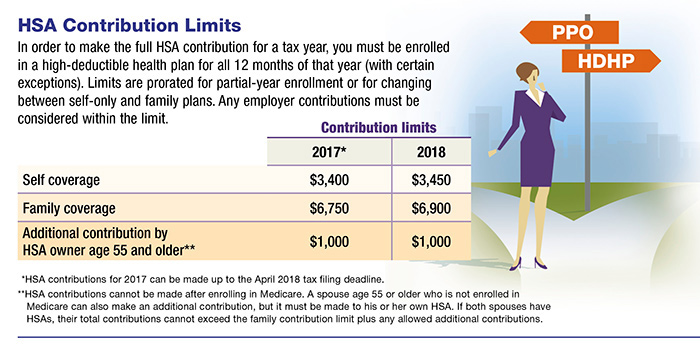

High-deductible health plans are designed to be paired with a health savings account (HSA), a tax-advantaged account that can be used to pay future medical expenses. HSA contributions are typically made through pre-tax payroll deductions, but in most cases they can also be made directly to the HSA provider. HSA funds, including any earnings if the account has an investment option, can be withdrawn free of federal income tax and penalties as long as the money is spent on qualified health-care expenses. (Some states do not follow federal rules on HSA tax treatment.)

HSA assets belong to the contributor, so they can be retained in the account or rolled over to a new HSA if you change employers or retire. Unspent HSA balances can be used to help meet medical needs in future years, whether you are enrolled in an HDHP or not; however, you must be enrolled in an HDHP to contribute to an HSA. Although HSA funds cannot be used to pay regular health insurance premiums, they can be used to help pay Medicare premiums and long-term care expenses.